Enterprise creation in biotech is witnessing a sustained contraction. After the pandemic bubble’s over-indulgence, the enterprise ecosystem seems to have reset its tempo of launching new startups.

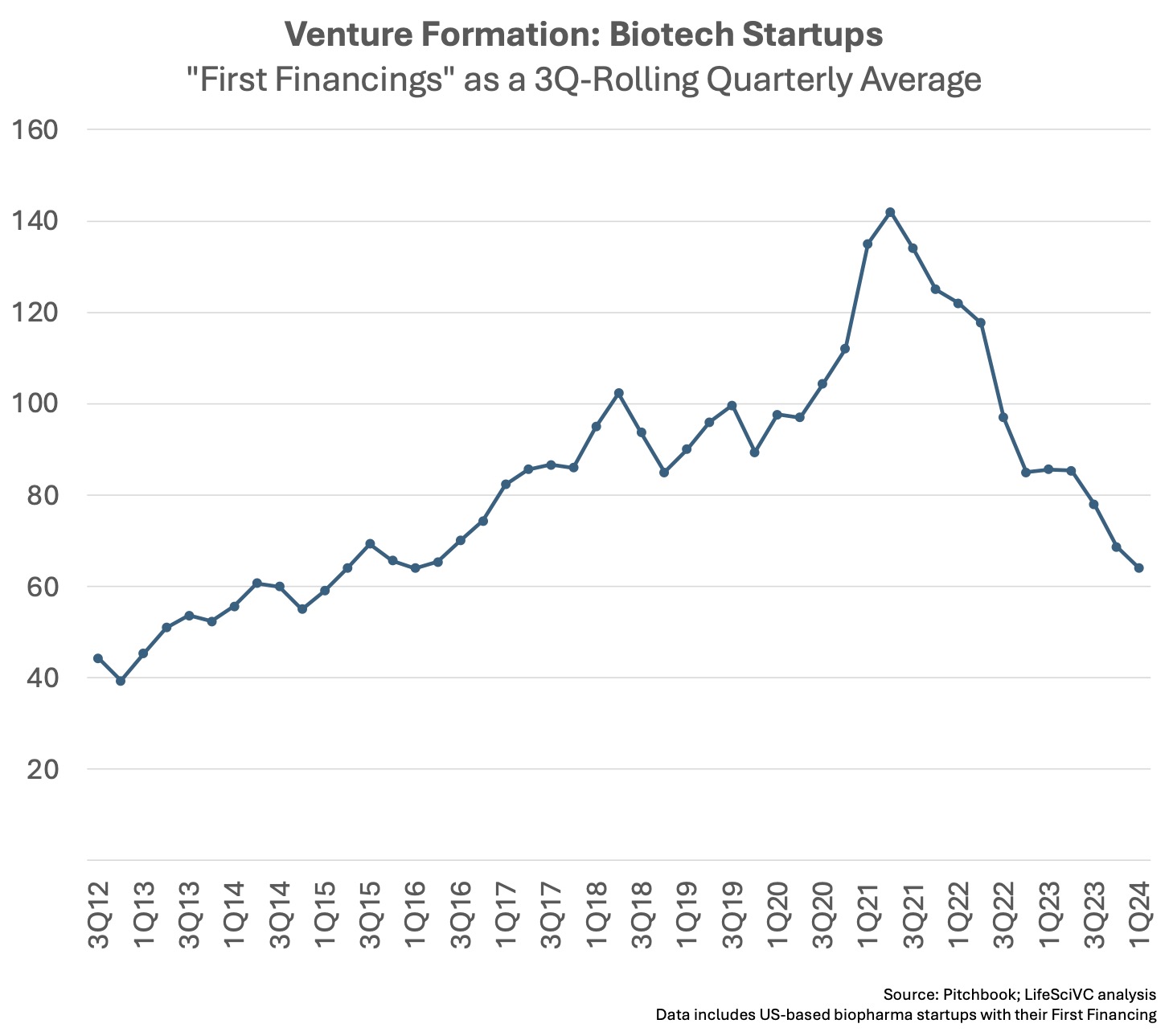

In line with the newest Pitchbook information, enterprise creation in biotech hit its slowest quarterly tempo in eight years throughout 1Q 2024. With simply over 60 new biotechs elevating their first spherical of financing, the sector’s firm formation exercise has slowed 50-60% from its historic peak in 2021.

{kind=link}

Total, this contraction is a powerful constructive signal of wholesome self-discipline, and must be good for the sector’s mid- and long-term prospects. Again in April 2023, within the midst of the second 12 months of the market pullback, I shared some reflections on why it was more likely to be “for the higher.” On the danger of revisiting these factors, listed below are a couple of causes for why I nonetheless imagine this contraction in enterprise creation is a wholesome dynamic for the sector:

First, enterprise creation is difficult to do properly, and even more durable at scale. Past merely backing nice science (separating the wheat from the chafe), setting an organization up correctly is important, and early selections can get locked into the DNA of the corporate. I’m typically reminded of Peter Thiel’s legislation: “A startup tousled at its basis can’t be fastened.” Again in 2013, I opined on this idea and lots of the pitfalls highlighted round messing up enterprise formation stay salient in the present day: unreproducible science (or poor goal choice), inexperienced founders/”founder-itis”, poor Board governance, unwieldy syndicates, odd founding agreements, off-market capitalizations, and so forth… These are all no much less related in the present day than up to now, and within the pandemic interval of irrational exuberance for giant science many startups integrated a number of these mutations into their founding DNA. Some proceed to take action in the present day, sadly, however there seems to be much less of it occurring.

Second, nice groups of actually skilled leaders are scarce. Catalytic executives, fairly than stoichiometric ones, can change the trajectory of startups however are in very brief provide. Some gray hair is usually, though not at all times, vital. Basically, even throughout tighter markets like in the present day, nice expertise is at all times a really constrained useful resource, and spreading it too thinly throughout too many firms isn’t good for the ecosystem. Nice scientists want nice enterprise companions, and vice versa, with the intention to be efficient leaders in biotech – which signifies that concentrating the scarce high-quality expertise in fewer firms will collectively be factor for the sector.

Third, with the proliferation of startups, we’ve seen unimaginable crowding in hyper-competitive therapeutic classes and modalities. This has lengthy been a characteristic of biopharma (see 2012 and 2016 posts on oncology and immune-oncology, respectively), however has been exacerbated by the creation of so many new firms. Additional, this lemming problem has additionally moved properly past oncology – consider all of the “not-so-fast follower” autoimmune packages or metabolic illness tales. Whereas it could assist shake out some incremental advances for the therapeutic armamentarium, this dynamic additionally clearly creates inefficiencies and waste – each by way of capital deployment, but additionally for sufferers’ engagement and medical trial exercise. Additional, the aggressive depth in sure areas makes the “medical do-ability” too difficult, even when these medicine might seemingly be useful. Fewer startups over time ought to ameliorate this crowding dynamic to some extent.

Fourth, the enterprise exit surroundings circa 2027-2030 for the brand new crop of early stage startups being created in the present day will seemingly have structural provide/demand components extra favorable than the backdrop lately. With enterprise creation exercise peaking in 2020-2022, the sector was awash in too many startups – very similar to the tech VC sector a couple of years again. In macroeconomic phrases, a glut of startup fairness (over-supply) within the face of fastened demand (M&A), or much less demand (IPOs), means an unfavorable pricing dynamic. I explored this in a unique part of the biotech enterprise cycle a decade in the past, however the themes are nonetheless related (in the wrong way) for describing the latest and difficult exit surroundings. With fewer startups being created, the provision/demand steadiness ought to revert to a extra favorable macro bias within the coming years (as soon as the pig has been digested). This, in fact, is just a touch upon ecosystem “flux” dynamics, not all the different potential coverage and pricing headwinds.

One important caveat to those constructive observations: our job is to carry medicines to sufferers. A extra constrained startup world means fewer bench-to-beside efforts might be launched into by the sector as an entire, which might depart modern new medicines stalled in laboratories world wide. We should be conscious of this problem, and be sure that one of the best concepts (fairly than simply one of the best related concepts) are getting superior by the sector.

It’s additionally vital to notice that my reflections above, and the info, are targeted on the variety of new startups being fashioned. Absolute funding ranges are vital too. Whereas additionally off from their peaks in 2021, there’s nonetheless important combination enterprise funding flowing into the startup world by any historic metric. Prior to now couple months, we noticed the primary $1B preliminary financing in biotech with the launch of Xaira, in addition to massive first financings from Metsera ($290M) and Mirador ($400M). Regardless of these mega-round financings, although, the median first financing stays within the $5-10M vary, the place it has been for years.

Stepping additional again to the asset class, this contraction must be considered positively by LPs, who make investments into enterprise funds, and the VCs they again, as extra self-discipline ought to translate into higher returns in the long run: constrained assets ought to enhance the common well being of the enterprise herd.

{kind=link}