{kind=link}

Within the custom of earlier fast S-1 teardowns (Snowflake, Palantir, Cerebras, and so on), some fast notes on the CoreWeave S-1 from my colleague Aman Kabeer and I. As in prior efforts, this isn’t meant to be 100% complete (and it’s actually not funding recommendation!).

The CoreWeave IPO goes to be fascinating to look at: partly as a result of it’s undeniably thrilling, and partly as a result of it’s not going your normal tech IPO. It presents a profile that in some methods is typical of a hyper-growth tech unicorn (explosive development, giant losses, dual-class inventory construction with Class A/B shares, and so on.), however in different methods, it’s very not like most tech IPOs of the previous. Its specialised enterprise mannequin, heavy infrastructure focus, heavy buyer focus (Microsoft), reliance on massive companions (NVIDIA), monetary construction ($10B in debt) and weird danger components make it a singular case that blends the traits of a cloud supplier, a {hardware} firm, and a startup driving an thrilling but additionally sudden and unproven market wave.

SOME KEY TAKEAWAYS

Frivolity: Crypto pivot, NJ in da home: For all of the jokes on social media about founders, startups and VCs pivoting from Web3 to AI, CoreWeave is an instance of a enterprise that began as a crypto mining operation, stockpiled GPUs, and pivoted to AI with spectacular success.

In the identical (frivolous) vein, for all of the “all AI is in SF” mantra, CoreWeave is headquartered in… New Jersey.

The First Generative AI IPO: Relying on pricing, there’s probably going to be large curiosity within the IPO. That is partially due to the well-documented dearth of tech IPOs, however most significantly as a result of it’s the primary IPO of the Generative AI period (Cerebras, so far as we all know, continues to be caught in CFIUS evaluate of their relationship with G42).

There are only a few “AI pure performs” on public markets – Palantir is one instance (cue within the by no means ending dialogue as as to whether they’re really an AI firm), as is (much more arguably) C3 AI. Aside from that, the best way to “play” Generative AI has been to put money into Magazine 7 corporations.

It’s no accident that the primary corporations to file S-1s within the Generative AI period are infrastructure corporations. The market has been forming supply-first (chips, information facilities, basis fashions), with the foremost hope that the demand facet surfaces equally meaningfully in years to come back.

Not a Actual Property Play: A unfavourable tackle CoreWeave and comparable corporations one would typically hear in tech circles is that the corporate is a “actual property play”, with restricted expertise and software program. The argument appeared to be supported by the truth that the co-founders of the corporate come from a monetary, quite than technological, background.

In its S-1, CoreWeave does a robust job dispelling that notion, positioning itself because the “AI Hyperscaler”. The present hyperscalers had been constructed “to host web sites, databases, and SaaS apps which have essentially totally different wants than the excessive efficiency necessities of AI”, therefore a “large want” for a purpose-built AI cloud platform, together with the infrastructure and built-in software program.

Its potential acquisition of Weights & Biases appears to verify its main push in direction of being a software program participant.

Explosive Income Development: The Generative AI period actually has seen its share of unbelievable development tales (OpenAI, Cursor, and so on), however they really pale compared to Coreweave’s development – from about $15.8 M in 2022 to $228.9M in 2023, after which $1.92B in 2024, a outstanding +737% Y/Y development final 12 months,, reflecting surging demand for AI compute providers

Massive (and Rising) Losses: On the similar time, CoreWeave stays deeply unprofitable. It incurred a web lack of $31M in 2022, which widened to $593.7 million in 2023 and $863.4 million in 2024 (-45% margin). In different phrases, bills grew nearly as quick as income – the 2024 web loss was about 45% of income (an enchancment from 2023, when the online loss exceeded 2× annual income).

Margins and Price Construction: CoreWeave’s gross margin is excessive (74% in FY’24), indicating that offering GPU compute at scale may be fairly worthwhile earlier than overhead. Nonetheless, working bills and different prices are large – together with depreciation of high-priced {hardware}, information middle operations, and curiosity on debt – resulting in unfavourable working margins. In brief, the core service is high-margin, however the heavy infrastructure investments and financing prices presently outweigh these good points.

For instance of large funding required: the spectacular quantity of fiber buildout to assist even a single 32K GPU cluster (~600 mi of fiber cables, ~80K fiber connections). In some ways, this resembles the bodily buildout required to assist the dot com period

That stated, given capital depth of the enterprise, with excessive non-cash bills (D&A, Loss on Truthful Worth Changes) driving GAAP effectivity down, the corporate is definitely extremely environment friendly on a non-GAAP foundation, with ~$1.2B in Adj. EBITDA in FY’24 (~64% Margin)

The Coreweave IPO might be an fascinating bellwether for the place public markets lean on Rev. Development vs. [GAAP] Effectivity Query

Buyer Focus: CoreWeave’s income is extremely concentrated in a number of giant prospects. Notably, Microsoft accounted for ~62% of CoreWeave’s income in 2024

– a particularly giant single-client share. A handful of different tech and finance corporations (equivalent to Meta, IBM, and hedge fund Jane Avenue) make up a lot of the remaining income, which means the corporate is determined by a small variety of massive spenders. This focus presents a danger: the lack of any main buyer (or perhaps a cutback of their utilization) would have a fabric affect on income. The IPO submitting highlights this reliance as a key danger, as such heavy dependence on one or two prospects is uncommon for an organization of this scale.

Lengthy-Time period Commitments and Enlargement Movement

Present buyer base of AI Labs / Mannequin Builders & AI Enterprises (MSFT, NVIDIA, IBM, Meta, and so on) do not make short-term bets, with multi-year agreements with CoreWeave as proof.

$15.1B in Remaining Efficiency Obligations (RPO) as of 12/31/24 & 4-year weighted common contract size

Dedicated contracts comprised an astonishingly excessive 96% of FY’24 Income

As well as, the enlargement movement is already working.

“Three of our prime 5 dedicated contract prospects by TCV as of December 31, 2024 signed agreements for extra capability inside 12 months of their respective preliminary buy dates. These agreements, measured throughout every respective 12-month interval from the preliminary date of signing, characterize a cumulative improve of roughly $7.8 billion in dedicated spend and a a number of of roughly 4x on preliminary contract worth.”

True Enterprise AI just isn’t right here but

What does the CoreWeave S-1 inform us concerning the actuality of the enterprise AI market?

As famous above, the important thing prospects are different infrastructure and expertise suppliers – MSFT, Meta, NVIDIA, IBM

For the remaining, it’s nonetheless early. From the S-1:

“Lengthen into broader enterprise prospects throughout new industries and verticals, together with regulated industries like banks, high-frequency buying and selling, and pharmaceutical corporations, as they start to develop and construct their very own devoted AI options. We anticipate that new industries and use circumstances will come up to benefit from growing AI capabilities as AI fashions change into extra accessible and cheaper, presenting extra development alternatives for our platform.”

“As AI continues to seek out product market match, we count on these enterprises to develop their oblique consumption of our platform by AI labs”

Provider Dependence (NVIDIA): CoreWeave is sort of completely depending on Nvidia for present and future GPUs. Any disruption in Nvidia’s provide chain, a call by Nvidia to prioritize different consumers, or Nvidia’s pricing energy might harm CoreWeave. Moreover, if Nvidia’s GPU expertise had been to fall behind or various AI chips rise, CoreWeave’s single-vendor technique might go away it weak. This “all eggs in a single basket” provide method is a key danger (particularly given how vital GPUs are to the enterprise).

ADDITIONAL NOTES

Firm / Background

- CoreWeave was based in 2017, initially as a crypto mining firm ‘Atlantic Crypto’, by Michael Intrator (CEO), Brian Venturo (Chief Technique Officer) and Brannin McBee (CDO)

- Rebranded in 2019 to CoreWeave and pivoted into offering compute assets forward of the AI growth, given current stockpile of GPUs for his or her mining operations

- CoreWeave is constructing the ‘AI Hyperscaler’, offering cloud-based GPU computing assets, storage & purpose-built software program providers for AI-native workloads & purposes. Three key parts underpin CoreWeave’s full stack GPU cloud platform:

- Infrastructure Companies – entry to GPU & CPU compute, with high-performance networking purpose-built for AI workloads, and storage

- Managed Software program Companies – Managed Kubernetes environments, VPC providing & naked steel providing

- Utility Software program Companies – SUNK (means to intelligently schedule jobs on prime of Kubernetes on a single cluster), CoreWeave’s proprietary Tensorizer (effectivity & mannequin loading optimizations) & inference optimization providers

- CoreWeave’s information middle community, with 27 places within the US & 4 places in Europe (enlargement in 2024), is optimized for AI-specific workloads. Firm advertises as much as 20% enchancment on MFU vs. current hyperscalers

Financials

GAAP

- Income

- FY’24: $1.9B (+737% Y/Y)

- FY’23: $229M (+1346% Y/Y)

- Gross Margin

- FY’24: $1.4B (~74% Gross Margin)

- FY’23: $160M (~70% Gross Margin)

- Working Earnings

- FY’24: $324M (~17% Margin)

- FY’23: $(14.5)M (~(6)% Margin)

- Web Loss

- FY’24: $(863)M (~(45)% Margin)

- FY’23: $(594)M (~(259)% Margin)

Non-GAAP & Money

- As highlighted above – firm has a number of giant non-cash bills owing to capital intensive & asset-heavy nature of the enterprise (excessive D&A) in addition to capital construction and valuation historical past (excessive Loss on Truthful Worth Changes) contributing to vital web loss on GAAP foundation

- Adj EBITDA

- FY’24: $1.2B (+64% Margin)

- FY’23: $104M (+45% Margin)

- CFO

- FY’24: $2.7B

- FY’23: $1.8B

- Working FCF (CFO – Capex)

- FY’24: -$6B

- FY’23: -$1.1B

- Change in Money (together with Debt & Fairness raised to finance capex)

- FY’24: $1.6B

- FY’23: $473M

Stability Sheet

- At first look, the abstract BS upfront paints a troublesome image, with two key observations standing out:

- Simply ~$1.4B Money vs. ~$8B Whole Debt (~$2.5B present Debt)

- Detrimental Working Capital (i.e. Present Property

- That doesn’t paint the complete image of the enterprise, nevertheless, given the distinctive approach they’ve constructed their ‘just-in-time’ debt financing mannequin

- How does their debt financing work?

- CoreWeave’s Debt Financing, particularly their Delayed Draw Time period Loans (DDTLs), are collateralized in opposition to contracted buyer obligations. They’re solely taking up debt to match the CapEx wanted to construct in direction of precise obligations laid out in signed contracts

- CoreWeave solely purchases tools after the shopper is contracted (i.e. they’ve buy orders to satisfy buyer contracts / obligations able to go, however don’t really make the acquisition till demand is firmed up)

- Buyer Contracts / Outlines Obligations → Purchase & Construct In direction of Obligations

- Timing Issues – Curiosity expense issues are mitigated by the truth that it’s a DDTL, which means you solely pay curiosity on the drawn quantity at any given time

- You possibly can draw the DDTL at will to construct in direction of contracted obligations, however as you try this & meet every milestone you additionally acknowledge requisite Income

- RPO (Remaining Efficiency Obligations), & RPO Development particularly, is the important thing metric to measure CoreWeave’s monetary well being

- $15.1B of RPOs ending FY’24 (+53% Y/Y)

Capital Construction

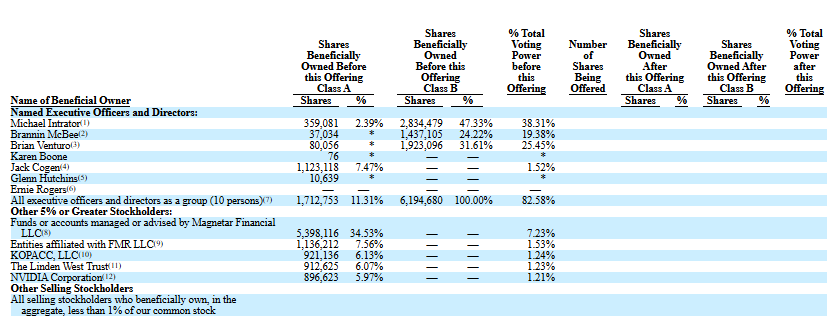

- Co-Founders bought ~$500M in Class A shares in a secondary in late 2024, nevertheless given Class A / Class B construction (Class B – 10x voting energy) nonetheless retain majority management of the enterprise

- Magnetar is the most important single shareholder within the enterprise, with ~35% possession

- Constancy (which was a big purchaser within the secondary) is the second largest institutional shareholder, with ~8% possession

{kind=link}