Abstract

This essay argues that conventional EA improvement practices, which regularly depend on excessively lengthy studying intervals, can result in overfitting and hinder efficiency in dynamic markets. By specializing in short-term optimization and steady adaptation, merchants can create extra strong and worthwhile EAs. The secret is to constantly refine the EA’s parameters primarily based on latest market knowledge, conduct rigorous out-of-sample testing, and implement strong danger administration methods. This strategy permits EAs to higher adapt to evolving market circumstances, resulting in improved efficiency and decreased danger.

Introduction

Knowledgeable advisors (EAs) goal to seize the inherent behavioral traits of buying and selling devices. Efficient EAs depend on correct understanding of those traits, which necessitates steady studying from historic knowledge. Nonetheless, the prevailing apply within the MQL5 neighborhood emphasizes excessively lengthy studying intervals, typically spanning a number of years. This strategy, whereas seemingly offering a way of safety, can result in overfitting and hinder adaptability to evolving market dynamics.

The Perils of Lengthy-Time period Studying:

Overfitting

Lengthy studying intervals enhance the chance of overfitting, the place the EA turns into overly attuned to previous market circumstances, together with anomalies and noise. This can lead to poor efficiency when market circumstances change.

False Sense of Safety

Presenting a long time of backtest outcomes with seemingly secure fairness curves can create an phantasm of security. Nonetheless, these outcomes might not precisely replicate real-world efficiency, particularly in unstable or quickly altering markets.

Historical past Studying, Not Future Forecasting

EAs educated on excessively lengthy intervals typically turn out to be “historical past readers,” successfully memorizing previous worth motion fairly than figuring out and adapting to evolving market patterns.

Large Cease-Losses Excessive Danger of Blowing Accounts

A good portion of MQL5 customers doesn’t t adequately take a look at or optimize their EAs. Let’s take into account an EA that displays a most drawdown of $1400 over the previous 5 years. This could ideally symbolize our most acceptable danger.If this EA encounters vital losses, we must always adhere to our stop-loss (SL) order till the utmost drawdown of $1400 is reached or exceeded. Nonetheless, human psychology typically tempts us to carry onto positions longer than we must always, hoping for a restoration.

What if our long-term backtesting was inaccurate, and the true most drawdown of the EA exceeds $1400? This might result in vital and sudden losses, probably jeopardizing the complete buying and selling account. This situation carries a considerable danger of great account losses.

By fastidiously contemplating danger parameters and conducting thorough backtesting, we are able to attempt to reduce these aggravating conditions and improve our buying and selling expertise

The Case for Quick-Time period Optimization:

Adaptability to Evolving Markets

Specializing in shorter studying intervals, reminiscent of 5-6 months, permits the EA to adapt extra successfully to latest market tendencies, together with short-term cycles, news-driven volatility, and shifts in market sentiment.

Diminished Danger

By specializing in latest market conduct, the EA can higher assess and mitigate present dangers, reminiscent of sudden market shifts or unexpected occasions. This could result in extra real looking danger administration and decreased drawdowns.

Improved Efficiency

By constantly adapting to altering market circumstances, short-term optimization can result in improved efficiency and probably increased returns in comparison with EAs educated on static, long-term knowledge.

Some Extra Issues:

The monetary markets are continually evolving. Components such because the conduct of market members, developments in buying and selling know-how, and shifts in financial circumstances are continually in flux. It is unrealistic to count on a single buying and selling algorithm to persistently seize the traits of a buying and selling instrument over prolonged intervals, reminiscent of 5 or ten years.

Even when an algorithm might obtain constant long-term efficiency, it might doubtless require vital constraints to mitigate the chance of overfitting to historic knowledge. This stringent strategy can result in a considerable discount in potential returns, leading to an unfavorable risk-reward profile.

This examine proposes a novel strategy to optimizing knowledgeable advisors, aiming to reinforce their efficiency and enhance danger administration.

Let’s delve deeper into this idea by inspecting the traits of its short-term cycles.

A Temporary Description of Quick Time period Cyclical Traits

Quick-term cyclical traits influenced by numerous components, reminiscent of macroeconomic knowledge releases, market sentiment, geopolitical occasions, and central financial institution coverage selections. These cycles are sometimes pushed by dealer psychology, market liquidity, and algorithmic buying and selling methods. Right here’s a breakdown of the standard traits and durations:

1. Intraday Cycles

Length: Hours to a single day.

Traits:

Usually pushed by market classes (e.g., Asian, European, and US buying and selling hours).

Volatility spikes throughout key market openings and main financial knowledge releases (e.g., nonfarm payrolls, ECB bulletins, or Fed rate of interest selections).

Patterns typically embody vary buying and selling throughout low-volume hours and breakouts throughout high-volume classes.

2. Multi-Day Cycles

Length: 2–5 days.

Traits:

Usually linked to short-term sentiment shifts, reminiscent of positioning forward of main financial or geopolitical occasions.

Contains patterns just like the “Monday impact” or reactionary actions following weekend information.

These cycles might replicate corrective strikes after robust tendencies or consolidations round particular technical ranges.

3. Weekly or Bi-Weekly Cycles

Length: 1–3 weeks.

Traits:

Might align with central financial institution assembly cycles, notably for the ECB or the Federal Reserve.

Displays market changes to modifications in financial coverage expectations or evolving macroeconomic knowledge.

Merchants typically refer to those as a part of a “mini-trend” inside a broader pattern.

4. Seasonal Cycles

Length: A number of weeks to months.

Traits:

Seasonal tendencies can come up attributable to recurring financial components, reminiscent of fiscal year-end flows, tax deadlines, or company repatriation.Mid-year and end-of-year intervals typically present distinct buying and selling patterns linked to portfolio rebalancing or hedging exercise.

By analyzing the short-term traits of worth motion, we are able to determine key cyclical patterns. If we choose a sufficiently lengthy studying interval, our EAs can probably be taught from these patterns, which usually embody:

Intraday cycles

Multi-day cycles

Weekly or bi-weekly cycles

Seasonal cycles

These cycles provide helpful insights into market conduct and may current potential buying and selling alternatives. Nonetheless, specializing in historic knowledge from 8 years in the past will not be related for present market circumstances. We have to prioritize studying from the latest worth motion to adapt to the evolving market dynamics.

Methodology:

1- Outline Studying Interval:

Decide an applicable studying interval. The examine above suggests sometimes 5-6 months studying interval ought to be sufficient. It could possibly be shortened with respect to desired buying and selling frequency and the instrument’s typical cycle durations.

2- Optimize:

Optimize the EA parameters inside the outlined studying window.

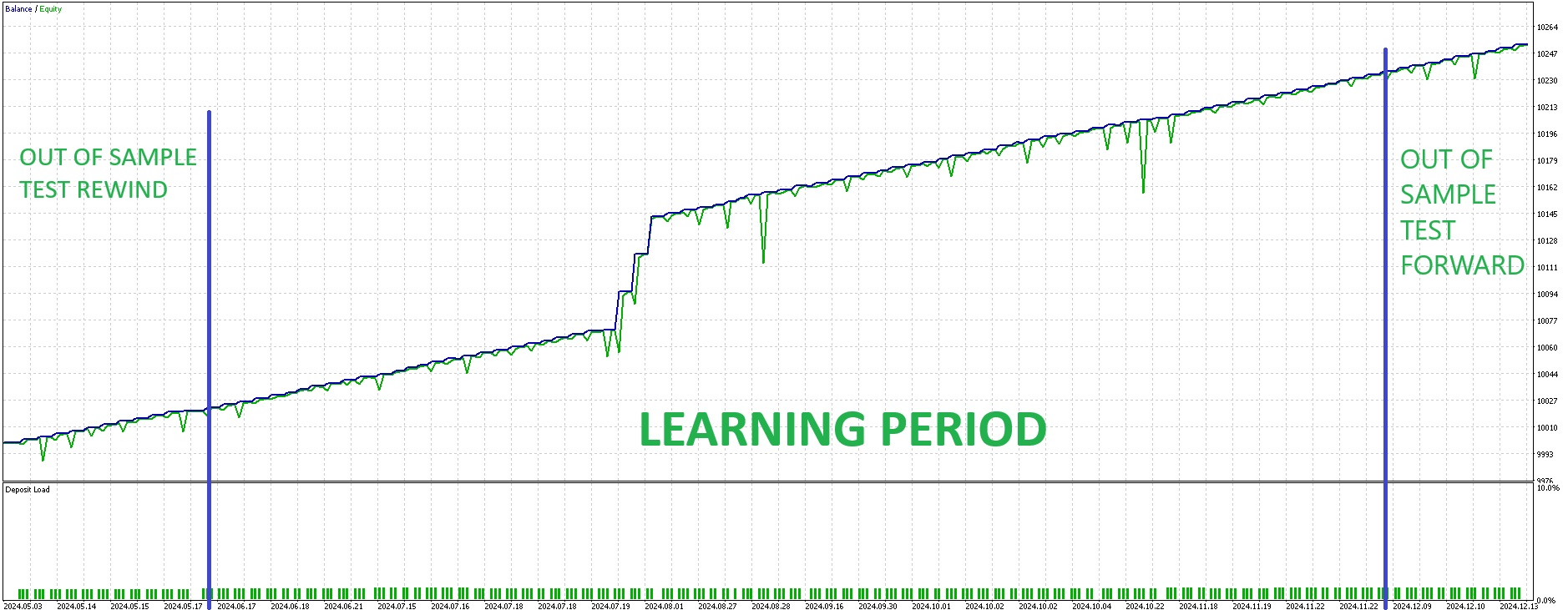

3- Out-of-Pattern Testing:

Conduct rigorous out-of-sample testing, together with ahead and rewind checks, to evaluate the EA’s efficiency on knowledge not used within the optimization course of.

4 – Common Re-optimization:

Re-optimize the EA periodically, ideally month-to-month or bi-weekly or much more continuously for high-frequency buying and selling methods, to make sure continued adaptation to evolving market circumstances.

THE APPLICATION

If at the moment is twenty first of December, we are able to setup our optimization routine as follows:

After we apply this strategy to a buying and selling algorithm, we have now the next fairness curve. Taking a look at it, this set file is accepted as a result of it performs effectively out and in of pattern checks.

How Ought to You Handle Your Danger?

Vital information occasions or financial knowledge releases can abruptly shift market sentiment, probably exceeding the scope of the educational interval for our EA.

Implementing a stop-loss (SL) order is essential for danger administration. The SL stage ought to be fastidiously decided to keep away from overly tight settings, which might result in frequent untimely exits, or excessively free settings, which can not adequately shield capital throughout adversarial market circumstances.

Ideally, the SL ought to be set to restrict potential losses to an quantity that doesn’t exceed a single day’s common revenue. As an illustration, in case your day by day common revenue is $40, the SL shouldn’t exceed this quantity.

Whereas some flexibility could also be potential when buying and selling solely with EAs, it is typically advisable to restrict the potential loss to not more than three days’ common revenue.

Accordingly, your EA parameters and place sizing ought to be adjusted to align with this danger administration guideline.

In our particular instance, we must always implement a stop-loss order when the drawdown (DD) exceeds $45, with a slight buffer for extra security. It is essential to notice that the long-term most drawdown (DD) for this knowledgeable advisor might probably attain $700 and even $800. By shifting our focus to short-term optimization and adapting to latest market circumstances, we have now considerably decreased the potential for substantial drawdowns. This strategy prioritizes danger administration and goals to reduce the influence of sudden market occasions on the buying and selling account.

Conclusion

By embracing short-term optimization and specializing in latest market conduct, merchants can improve the adaptability, efficiency, and danger administration of their EAs. This strategy requires a extra proactive and dynamic strategy to EA administration, however it will probably in the end result in extra strong and worthwhile buying and selling methods.

{kind=link}